.png?width=2688&height=1120&length=2688&upsize=true&upscale=true&name=How%20Do%20You%20Make%20the%20Best%20Use%20of%20Extra%20Money%20(like%20a%20Financial%20Windfall).png)

Latest Posts

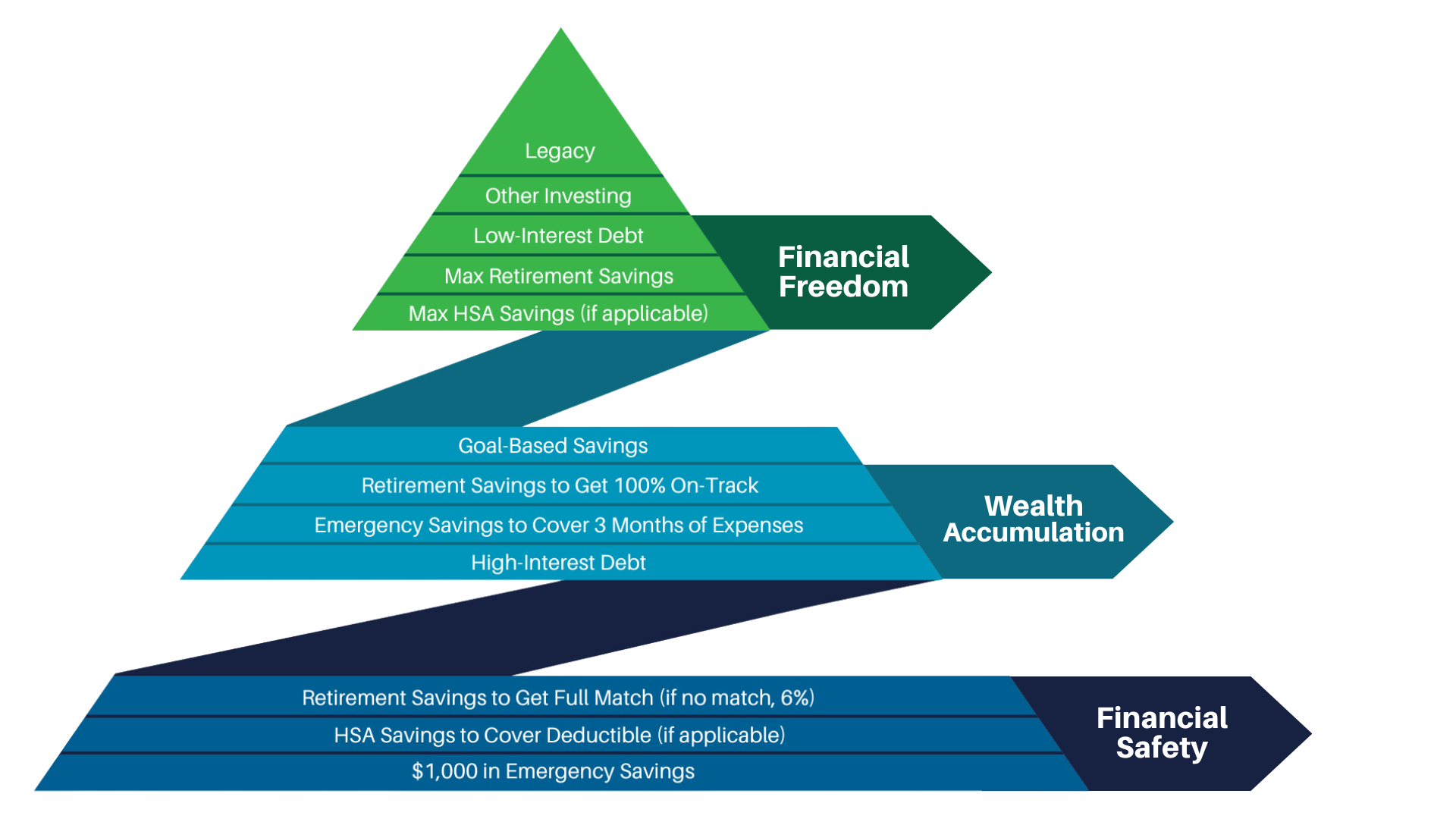

Let’s say you have a “financial windfall,” or perhaps have some extra money you have accumulated and are trying to figure out what you should do with this money. Before jumping into an investment or spending the money to “treat yourself,” the first step requires assessing your current financial situation. With that in mind, there are three areas in our Hierarchy of Financial Needs for you to consider:

With that in mind, there are three areas in our Hierarchy of Financial Needs for you to consider:

- Emergency savings

- Debt management

- Medium or long-term financial goals.

If you have these foundational pieces in place, then you can consider investing the extra money in something else. However, if you lack emergency savings or have high-interest debt, prioritize those areas first. In this Money Hacks episode, we suggest determining if you are on track with a strong financial foundation first and try making wise financial decisions for today, tomorrow, and your long-term future.

Any money questions you’d like answered? Our Money Hacks series is created from conversations we have with employees, investors, savers, and all people planning for their financial futures. What topics are on your mind for our next episode?

Video Transcript:

Hey, this is Alex Assaley and it's episode 104 of Money Hacks, as we wind down the first quarter of 2023, we continue to have some volatility and ups and downs in the financial markets. We've been getting a lot of questions in one-on-one coaching sessions with employees, particularly around how to invest when you have an extra kind of financial windfall, when you have extra money that you've either, you know, get a bonus or maybe your tax refund, we'll talk about whether or not that's a good thing in another video, uh, or just accumulated some extra money that you're looking to put to work, you're looking to use in the most efficient way. So, said another way, what do I do with a financial windfall?

I think our, best piece of advice is to think about where you are in your financial picture and one of the things, we've built is this hierarchy of financial needs. It's on our website, MoneyNav.com, you can check it out to see, you know, where you stand when it comes to these different components of your financial life.

And if you have the foundational pieces in place. Specifically, I wanna talk about three areas of that hierarchy. So, the first one is around short-term emergency savings, so money that you're gonna need for an unexpected expense, a financial emergency, or a short-term goal that might occur in the next zero to three years.

The second piece is debt management, ensuring that high-interest or bad debt is getting paid down or paid off. And then the third piece is longer-term financial goals. So, this could be things like retirement savings or non-retirement savings for financial priorities or life milestones that are, let's say, three to 10 or 15 years down the road.

If you have this financial windfall and you're looking to try to optimize what you're gonna do with, with this money that you've accumulated, I think assessing each of those three areas and determining if you are on track or if you are aligned with some kind of good financial guidance within those areas.

So, for example, have you built up three months or three to six months' worth of emergency savings? If you're on track there or in a good shape there, then you don't necessarily need to use that financial windfall to apply toward that bucket. But if that's an area of focus or that you need to improve, that might be the first place you put those assets.

The second one you know, is around debt management. Do you have high-interest debt? Things like credit cards, personal loans, and perhaps student loans that are creating a drag on your cash flow where you're paying higher rates of interest every month on those payments kind of eating away at cash flow you would otherwise have and if so, I would say that once you get the emergency savings piece in place, any extra, assets that you have from a financial windfall should go towards paying down or paying off that high-interest debt that may not seem like a big deal, but over time is really creating an extra drag on your financial picture.

It ends up being pretty large sums of money over the course of a year, a few years that you're paying interest to service or finance that debt. If you have those two pieces in place, look towards longer-term financial goals or financial milestones. This is money that you're not gonna use in the next three or four years, and then it gives you the ability to invest that money and try to get some, appreciation and return over a longer period of time, a five, 10 plus year time horizon. Sometimes investors who, have this additional money want to immediately try to put it into the markets immediately, and get some quick, performance growth on it, or appreciation on it, which carries a significant amount of risk and, a low probability for success on a year-by-year basis.

When there are these other areas of their financial life that would be, much better options in terms of how to use that money. So, I hope this video helps. You can find more on MoneyNav.com when it comes to our hierarchy of financial needs, sort of our belief around making wise financial decisions for today, tomorrow, and your long-term future. So, check it out there and we'll see you next time.